When it comes to your finances, your credit score is one of the most important details for you to keep track of. It can limit what you’re able to buy; and on loans, it can control how much you pay in interest. The easiest way to track your credit is by following your FICO, short for Fair, Isaac and Company, score. A FICO Score combines multiple reports into one to give a single score. Many institutions rely on this score to gauge risk associated with giving you a loan or issuing credit. In this article, we’ll tell you what you need to know about FICO Scores to help you now and in the future.

Why is a FICO Score important?

There are countless reasons why a FICO Score is important, but the most important may be its reputation. As previously mentioned, FICO is used by many institutions to determine the risk associated with lending you money. If you are going to buy a car, a home, or even shop around for insurance, your FICO Score will be one of the factors used to determine your eligibility and your interest rate on a loan. A poor or low score could mean you pay more than you typically would need to, aren’t approved at all or are approved but at a very high interest rate.

What are the factors that help determine my score?

We’re glad you asked! There are 5 key factors that help contribute to your FICO score. Each one has a different weight. The chart below has each factor, and the weight it has on your score listed. To make sure you have a full understanding, we’ll explain each factor in a little more detail.

Payment History

Payment history factors in to any late payments you make on any bills, credit cards or loan payments as well as if you have ever filed for bankruptcy. It has the most weight on your credit because it shows how likely the institution backing the credit is to get their payment. That is why it is essential to your credit that you stay on top of all your payments.

Utilization

This is a determination of how much you owe. And a key reason why it is important to keep your credit balances low and avoid taking out loans when you can. If you have high credit balances it will negatively affect your score. One rule of thumb that you want to keep your credit balances at about 30% or less of the total credit available. Obviously, the closer to zero the better, but with credit utilization being 30%, keeping credit balances low will be important to maintain a good score.

Length of Credit History

This is why it is important to get a credit card when you are young. It is also the easiest way to build a history. The longer you wait the more difficult it will be for you to get loans approved. If you’re looking for places you can start building credit, consider a secured credit card. If you already have a head start giving you multiple sources of credit, the average length is what is used as the actual length of your history.

Recent Activity

I’m sure someone at some point has told you to limit the number of inquiries service providers and lenders pull on your credit. Don’t apply for loans you don’t anticipate following through on. While it is always good to shop around, being smart and doing your own research first can help limit the number of applications you need to submit.

Credit Mix

This final factor has to do with how many active loans and credit accounts you have. It is only 10% of what is factored in, but you will still want to keep this in mind.

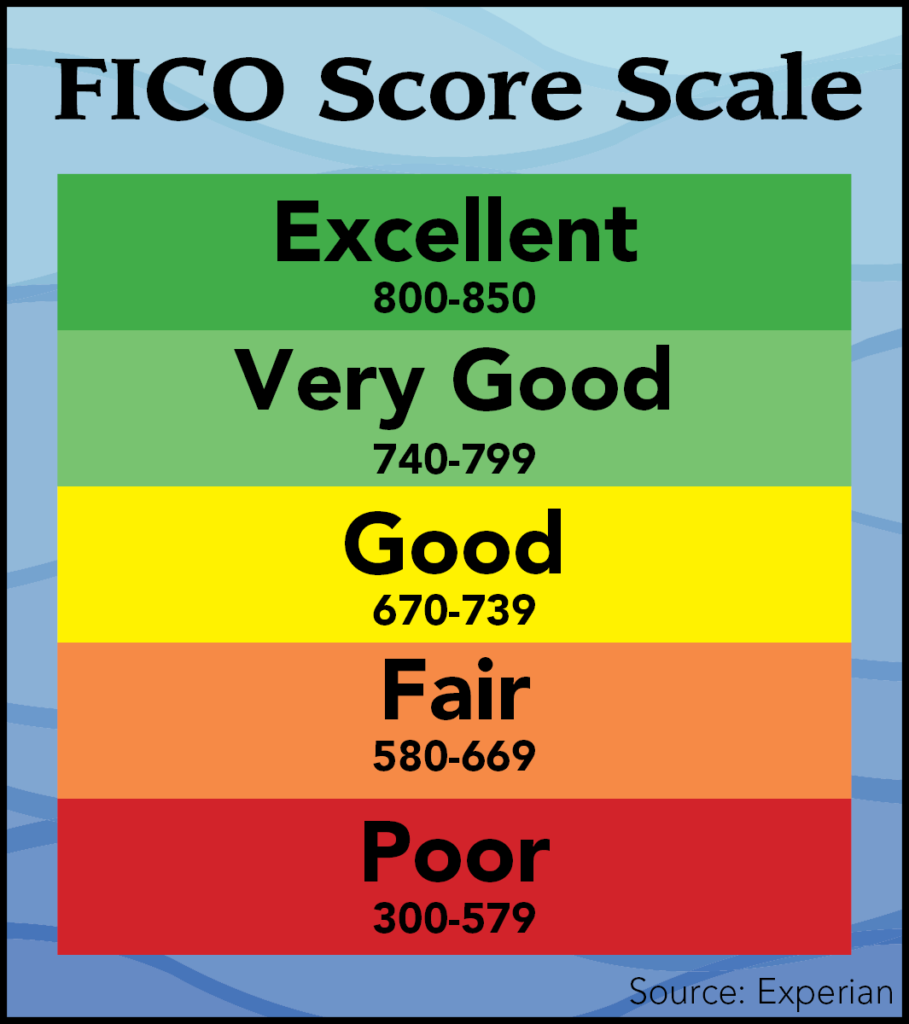

What are the score ranges?

Scores range from 300-850 as noted in this chart. The average score in America is a 700. While you may already know your score, or have a source that gives you the score, you are entitled to a free credit report every 12 months from each of the three major credit bureaus. To see how you compare, you can pull your credit from www.annualcreditreport.com/. If you’re using it to monitor fraud, we recommend alternating between bureaus every three to four months and tracking your results. This website is endorsed by the Federal Trade Commission. Currently, the major credit bureaus charge if you want to see your credit score, but there are some notable free services out there which provide your score at no charge.

If you are interested in checking your score check out Credit Karma or Credit Sesame. If your score needs a boost, check out our lending options here at https://centralnational.com/personal/lending.asp or just stop by one of our branches to visit with a lender today.