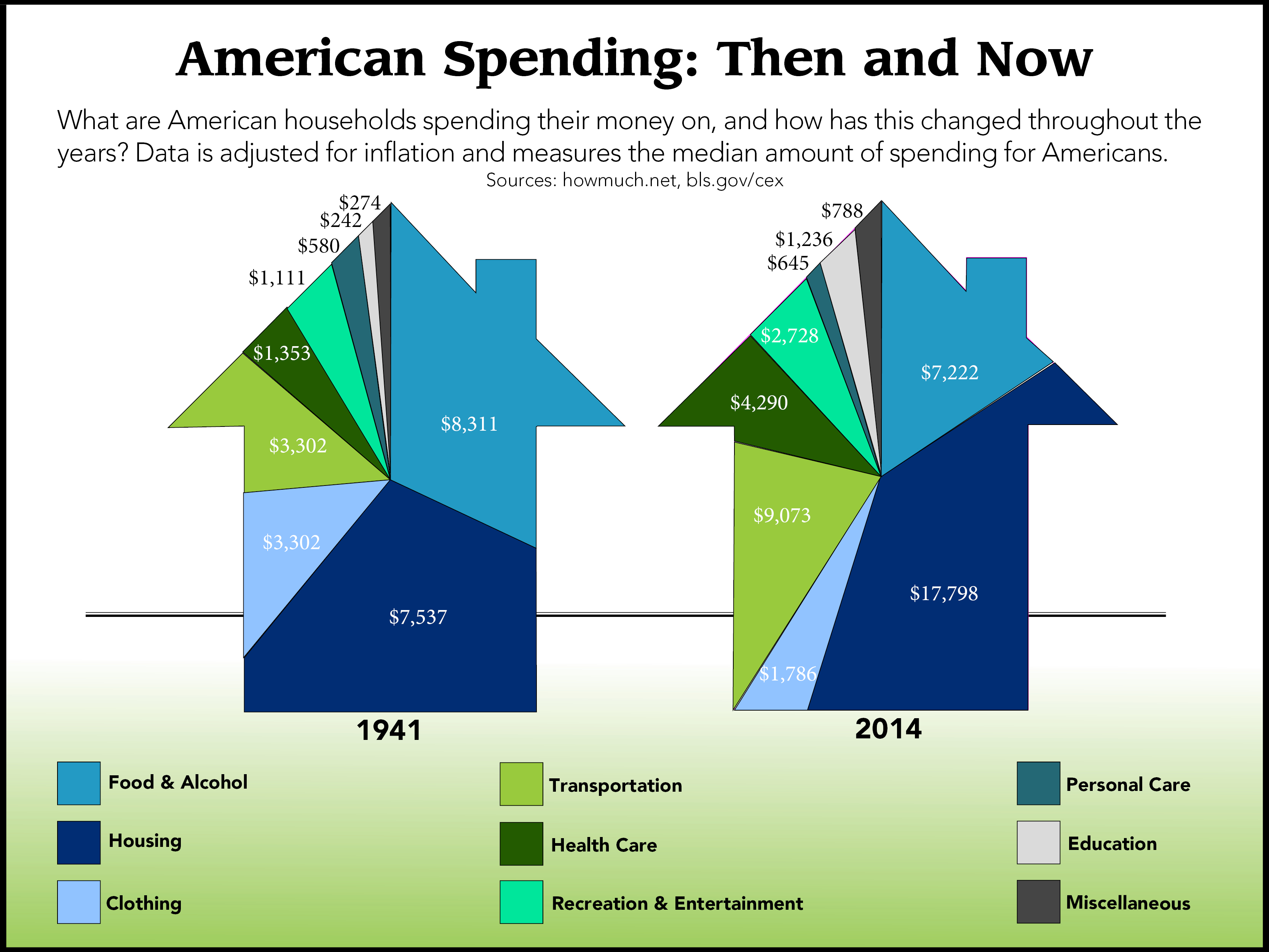

With Autumn finally here, the only thing falling should be the leaves – not your bank account! While everyone’s bound to make a financial mistake or two, there are some common problems that you can avoid in order to keep your future secure. We’ve created a list of eight major money mistakes that can add up to serious financial trouble (and steps you can take to begin fixing them).

1) Not having a budget

While it may seem obvious that you can’t live beyond your means if you want to save money, this is often easier said than done. Many people don’t realize exactly how much they’re spending on small, everyday items such as that morning cup of coffee. Additionally, if you use a credit or debit card most of the time, it’s even easier to spend money without realizing how often or how much. Instead, try to limit yourself to a certain amount of cash per week, so you know exactly how much you’re spending.

Tip: Create a spreadsheet with all your expenses, loans, assets, etc. Then break it down by day so you know how much you make (and can afford to spend) everyday.

2) Not having an emergency fund

2) Not having an emergency fund

This one is similar to not having a budget. According to a 2017 survey by Bankrate, 59 percent of Americans don’t have enough savings for an emergency expense. While experts usually recommend having at least 3 months of expenses saved (in liquid assets), this emergency fund calculator can help you get a better idea of what’s necessary for your situation. The best way to start saving for an emergency fund is to set aside a portion of your paycheck every month. Don’t forget, your fund should grow as your income and expenses do.

3) Not taking advantage of your employer’s 401(k) match

Many employers will match what you put into your 401(k) retirement plan up to a certain amount each year. This amount will vary, but you should always maximize it if you want to take full advantage of free money. Make sure you know your company’s matching policy, and what you need to do to get this money.

4) Not having the right insurance

Insurance is not a one-size fits all plan. Depending on your situation, you might need whole life insurance (for your entire life) or just term insurance, which can cover shorter periods like 5 to 30 years. You should also decide what other types of insurance would be appropriate for you (such as disability, homeowners and auto) and understand all your current policies, how much they cover and what this includes.

Tip: Not sure where to start? You can request a quote from us here.

5) Not paying attention to your credit score

Credit score is often talked about because it’s so important. Looking to buy a car? Rent an apartment? Apply for a mortgage? These are all situations where your credit score is crucial to the kind of interest rates you can get, which will definitely affect your financial future. Be sure to check your credit score at all three major consumer reporting agencies at least once a year to make sure it’s in your expected range, and there are no mistakes on any of the reports. You can find other methods of fraud protection here. Also, be aware of what lines of credit you have available, as this can impact your score.

6) Not paying off debt ASAP (or in the right way)

It’s common for people to make minimum payments on their debt until they have a higher income and can start paying off bigger chunks at a time. However, you can’t guarantee that your income will increase (or know when it will), while your debt will definitely become more costly thanks to interest rates. To save in the long-run, pay off as much as you can, as soon as you can. Additionally, it’s important to be smart about how you’re paying off your debt. Pay down those with the highest interest rates first.

Tip: Credit cards, with rates typically in the teens, should be paid before mortgages, where rates stay under 5 percent.

7) Not diversifying

Having diverse assets is something that goes along with the “Don’t put all your eggs in one basket” advice. However, this is something that can get complicated, and not a lot of people are highly informed about it. Besides educating yourself (here’s a place to start), you can hire a financial adviser who can give you as little or as much help as you need. Here’s a simple example though: make sure that you’re not relying entirely on your 401(k) for retirement. Instead, have additional options like a Roth IRA that can reduce your future taxes.

8) Not buying used

Buying anything used will save you money that will add up to a nice chunk of change later. Of course, there are some things that you should buy new, but cars aren’t one of them. Despite being one of the first things that comes to mind when you hear “depreciating asset,” cars have become a status symbol for many people. For someone who can afford a new car and wants to spend their discretionary cash on one, this isn’t a problem. But for those who are struggling to save money, a new car is a huge financial drain. Instead, look into used cars before ruling them out entirely.